Interested to see our 4th Quarter Market Report? Download to read more.

Most of us would prefer not to think about an unexpected (and unwelcome) early retirement, but it does happen frequently. In fact, nearly half of current retirees retired earlier than planned, and of that group, more than 60% did so due to changes at their company or a hardship, such as disability.1 For that reason, it’s a good idea to take certain steps now to help prepare for the unexpected.

What you can do now

Save as much as possible in tax-advantaged accounts.

If you’re forced to retire earlier than planned, your work-sponsored retirement plans, IRAs, and health savings accounts (HSAs) could become critical resources. HSA assets can be used tax-free to pay for qualified medical expenses at any time, and you can generally tap your retirement plan and IRA assets after age 59½ without penalty. Although ordinary income taxes apply to distributions from pre-tax accounts, qualified withdrawals from Roth accounts are tax-free.2

In addition, the IRS has identified several situations in which retirement account holders may be able to take penalty-free early withdrawals. These include disability, terminal illness, leaving an employer after age 55 (work-based plans only),3 to pay for unreimbursed medical expenses that exceed 7.5% of your adjusted gross income, and to pay for health insurance premiums after a job loss (IRAs only).

Pay down debt.

Generally, it’s wise to enter retirement (especially when unexpected) with as little debt as possible. Ensuring that your financial plan includes a strategy for paying down student loans, credit card debt, auto loans, and mortgages can help you minimize your income needs later in life.

Know your bare-bones budget.

Another way to help cushion the shock of an unexpected early retirement is knowing exactly how much you spend each month on your basic necessities, including housing, food, utilities, transportation, and health care. Maintaining a written budget throughout life’s ups and downs will help you quickly identify how much income you’d need over the short term while you work on a longer-term income-replacement strategy.

Maintain adequate levels of disability insurance. Your employer may offer group coverage at reduced rates; however, you lose those benefits if your employment is terminated. Private disability income insurance can help you secure coverage specific to your needs, and since the premiums are typically paid with after-tax dollars, any benefits would generally be tax-free (unlike work-sponsored coverage that is paid with pre-tax dollars).

Understand Social Security benefits.

If you stop working due to disability, you may qualify for Social Security Disability Insurance benefits if you meet certain requirements. You must have earned a certain number of work credits in a job covered by Social Security and have a physical or mental impairment that has lasted or is expected to last at least 12 months or result in death. If you remain eligible, benefits may continue up to age 65 and then convert to Social Security retirement benefits.

If you need to retire earlier than planned for reasons unrelated to disability and are eligible for Social Security retirement benefits, you can apply as early as age 62. However, starting payments prior to your full retirement age (66 or 67, depending on year of birth) will result in a permanently reduced monthly benefit.

For more information on Social Security disability and retirement benefits, visit the Social Security Administration’s website at ssa.gov.

Consider your health insurance options.

Terminating employment prior to age 65 could leave you without health insurance. You may opt to continue your employer-sponsored health coverage for a limited period (permitted through COBRA, the Consolidated Omnibus Reconciliation Act), although this can be quite expensive. If you’re married and your spouse works, you may get coverage under their plan. You may also seek coverage through the federal or a state-based health insurance marketplace. If you receive Social Security disability benefits, you’d automatically qualify for Medicare after 24 months.

Why 49% of Retirees Retired Earlier Than Planned

Don’t be caught off guard

Don’t wait for an unwelcome surprise. Take steps now to help ensure your overall financial plan considers the “what-if” of an unexpected early retirement.

1) Employee Benefit Research Institute, 2024

2) Qualified Roth withdrawals are those made after a five-year holding period and after the account owner dies, becomes disabled, or reaches age 59½. The penalty for early retirement account distributions and nonqualified withdrawals from Roth accounts is 10%. Nonqualified withdrawals from HSAs will be subject to ordinary income tax and a 20% penalty. After age 65, individuals can take money out of HSAs penalty-free, but regular income taxes will apply to funds not used for qualified medical purposes.

3) Age 50 or after 25 years of service for public safety officers

IMPORTANT DISCLOSURES

The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Securities and investment advice offered through Investment Planners, Inc. (Member FINRA/SIPC) and IPI Wealth Management, Inc., 226 W. Eldorado Street, Decatur, IL 62522. 217-425-6340.

Remember when you turned 16 and rushed to get your driver’s license? Or earned the right to vote at 18 and enjoyed the privileges and responsibilities of adulthood at 21? There aren’t many legal changes associated with birthdays after that until you turn 50, and then there are plenty.

Can you match these ages to the related federal benefits and tax responsibilities? One age will be used twice.

50 55 59½ 62 65 67 70 73 75

___ 1. Eligible for full Social Security benefits for those born in 1960 or later

___ 2. Earliest age to make catch-up contributions to a traditional IRA or an employer-sponsored retirement plan

___ 3. Eligible for maximum Social Security benefit

___ 4. Must begin taking required minimum distributions from most tax-deferred retirement plans, for those born from 1951 to 1959

___ 5. Eligible to enroll in Medicare

___ 6. Earliest age to make catch-up contributions to a health savings account

___ 7. Earliest eligibility age to begin taking reduced Social Security worker benefits

___ 8. Must begin taking required minimum distributions from most tax-deferred retirement plans, for those born in 1960 or later

___ 9. Eligible to withdraw money from a tax-deferred IRA or employer-sponsored retirement plan (for most employees) without incurring a 10% federal tax penalty

___ 10. Eligible to withdraw money from a tax-deferred employer-sponsored retirement plan without incurring a 10% federal tax penalty, for an employee who separates from service with the employer

For further information, visit irs.gov, socialsecurity.gov, and medicare.gov.

Answers

1. 67; 2. 50; 3. 70; 4. 73; 5. 65; 6. 55; 7. 62; 8. 75; 9. 59½; 10. 55 (50 or after 25 years of service for qualified public safety employees)

IMPORTANT DISCLOSURES

The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Securities and investment advice offered through Investment Planners, Inc. (Member FINRA/SIPC) and IPI Wealth Management, Inc., 226 W. Eldorado Street, Decatur, IL 62522. 217-425-6340.

The Taxpayer Relief Act of 1997 provided homeowners who sell their principal residence an exclusion from capital gains taxes of $250,000 for single filers and $500,000 for joint filers. At that time, the average price of a new home was about $145,000, so this exclusion seemed generous and allowed more Americans to move freely from one home to another.1 Unfortunately, the exclusion was not indexed to inflation, and what seemed generous in 1997 can be restrictive in 2024.

Capital gains taxes apply to the profit from selling a home, so they may be of special concern — and potential surprise — for older homeowners who bought their homes many years ago and might yield well over $500,000 in profits if they sell. In some areas of the country, a home bought for $100,000 in the 1980s could sell for $1 million or more today.2 At a federal tax rate of 15% or 20% (depending on income) plus state taxes in some states, capital gains taxes can take a big bite out of profits when selling a home. Fortunately, there are some things you can do to help reduce the taxes.

Qualifying for exclusion

In order to qualify for the full exclusion, you or your spouse must own the home for at least two years during the five-year period prior to the home sale. You AND your spouse (if filing jointly) must live in the home for at least two years during the same period. The exclusion can only be claimed once every two years. There are a number of exceptions, including rules related to divorce, death, and military service. If you do not qualify for the full exclusion, you may qualify for a partial exclusion if the main reason for the home sale was a change in workplace location, a health issue, or an unforeseeable event.

Increasing basis for lower taxes

The capital gain (or loss) in selling a home is determined through a two-part calculation. First, the selling price is reduced by direct selling costs, including certain fees and closing costs, real estate commissions, and certain costs that the seller pays for the buyer. (The amount of any mortgage pay-off is not relevant for determining capital gains.) This yields the amount realized, which is then reduced by the adjusted basis.

The basis of your home is the amount you paid for it, including certain costs related to the purchase, plus the costs of improvements that are still part of your home at the date of sale. In general, qualified improvements include new construction or remodeling, such as a room addition or major kitchen remodel, as well as repair-type work that is done as part of a larger project. For example, replacing a broken window would not increase your basis, but replacing the window as part of a project that includes replacing all windows in your house would be eligible. This basis is adjusted by adding certain payments, deductions, and credits such as tax deductions and insurance payments for casualty losses, tax credits for energy improvements, and depreciation for business use of the home. (See hypothetical example.)

Hypothetical Example

Pete and Joanne purchased their home for $100,000 in 1985 and sold it for $800,000 in 2024. This is how their capital gains might be calculated.

This hypothetical example of mathematical principles is for illustration purposes only. Actual results will vary.

Inheriting a home

Upon the death of a homeowner, the basis of the home is stepped up (increased) to the value at the time of death, which means that the heirs will only be liable for future gains. In community property states, this usually also applies to a surviving spouse. In other states, the basis for the surviving spouse is typically increased by half the value at the time of death (i.e., the value of the deceased spouse’s share).

Determining the capital gain on a home sale is complex, so be sure to consult your tax professional. For more information, see IRS Publication 523 Selling Your Home.

1) U.S. Census Bureau, retrieved from FRED, Federal Reserve Bank of St. Louis, 2024

2) CNN, January 29, 2024

IMPORTANT DISCLOSURES

The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Securities and investment advice offered through Investment Planners, Inc. (Member FINRA/SIPC) and IPI Wealth Management, Inc., 226 W. Eldorado Street, Decatur, IL 62522. 217-425-6340.

The IRS recently released the 2025 contribution limits for health savings accounts (HSAs), as well as the 2025 minimum deductible and maximum out-of-pocket amounts for high-deductible health plans (HDHPs).

What is an HSA?

An HSA is a tax-advantaged account that enables you to save money to cover health-care and medical costs that your insurance doesn’t pay. The funds contributed are made with pre-tax dollars if you contribute via payroll deduction or are tax deductible if you make them yourself using after-tax dollars. Withdrawals used to pay qualified medical expenses are free from federal income tax.

You can establish and contribute to an HSA only if you are enrolled in an HDHP, which offers “catastrophic” health coverage and pays benefits only after you’ve satisfied a high annual deductible. Typically, you will pay much lower premiums with an HDHP than you would with a traditional health plan such as an HMO or PPO.

If HSA withdrawals are not used to pay qualified medical expenses, they are subject to ordinary income tax and a 20% penalty. When you reach age 65, you can withdraw money from your HSA for any purpose; such a withdrawal would be subject to income tax if not used for qualified medical expenses, but not the 20% penalty.

HSA contributions, earnings, and withdrawals may or may not be subject to state taxes; most states with an income tax follow the federal tax rules for HSAs.

What’s changed for 2025?

Here are the updated key tax numbers relating to HSAs for 2024 and 2025

IMPORTANT DISCLOSURES

The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Securities and investment advice offered through Investment Planners, Inc. (Member FINRA/SIPC) and IPI Wealth Management, Inc., 226 W. Eldorado Street, Decatur, IL 62522. 217-425-6340.

Scam artists often prey on those who are most vulnerable. Unfortunately, this includes individuals who have recently lost a loved one and are easily taken advantage of during their time of grief. Scammers will look for details from obituaries, funeral homes, hospitals, stolen death certificates, and social media websites to obtain personal information about a deceased individual and use it to commit fraud.

A common scam after the loss of a loved one, often referred to as “ghosting,” is when an identity thief uses personal information obtained from an obituary to assume the identity of a deceased individual. That information is then used to access or open financial accounts, take out loans, and file fraudulent tax returns to collect refunds. Typically, a ghosting scam will occur shortly after someone’s death — before it has even been reported to banks, credit reporting agencies, or government organizations such as the Social Security Administration (SSA) or Internal Revenue Service (IRS).

Another scam involves scam artists using information from an obituary to pass themselves off as a friend or associate of the deceased — sometimes referred to as a “bereavement” or “imposter” scam. These individuals will falsely claim a personal or financial relationship with the deceased in order to scam money from grieving loved ones. Scam artists will also pose as government officials or debt collectors falsely seeking payment for a deceased individual’s unpaid bill.

If you recently experienced the loss of a loved one, consider the following tips to help reduce the risk of scams:

IMPORTANT DISCLOSURES

The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Securities and investment advice offered through Investment Planners, Inc. (Member FINRA/SIPC) and IPI Wealth Management, Inc., 226 W. Eldorado Street, Decatur, IL 62522. 217-425-6340.

Traditionally, tipping has been a way to reward workers for providing good service. But the norms around tipping are changing, and if you’ve recently felt more pressure to tip, you’re not alone. A survey by the Pew Research Center found that 72% of adults said that tipping was expected in more places today than it was five years ago, a phenomenon known as “tip creep” or “tipflation.” 1

Why tipping culture is changing

Tipping affects everyone (even tipped workers have to tip others!) and confusion and complaints about tipping abound. If you’re among those feeling uneasy about tipping, blame the pandemic. That’s when tipping culture started to change. Consumers, anxious to reward front-line workers and support struggling businesses, left more and bigger tips. Businesses adopted digital ordering and payment solutions that made tipping more convenient and could be programmed with preset tip suggestions that were often higher than customers were used to.

And then inflation took its toll. Businesses that lost employees during the pandemic increasingly realized that tips could help fill wage gaps and attract employees reluctant to return to service positions. But consumers, already having to make their money go further, began to grow weary of seemingly constant tip requests, especially in situations or places where they had not previously been asked to tip.

To Tip or Not to Tip?

Source: Pew Research Center, 2023

Tipping guidelines

Tipping often feels good, but the pressure to tip can be guilt-provoking and confusing. When a worker turns a screen around and you’re prompted to choose a preset tip, it can feel wrong to choose the lowest option. While you might always tip your server at a sit-down restaurant, in situations where you’ve had little to no direct interaction with any employee, should you even tip at all?

Ultimately, tipping is always voluntary and it’s up to you to decide who, where, and how much to tip. While there are no set rules, here are some guidelines you can use to inform your decisions.2

Finding a balance

Planning ahead can help you avoid some of the frustration around tipping and still tip fairly and appropriately.

Do an informal audit. How much have you spent on tips during the last month or two? Does that align with your budget?

Set tipping limits you’re comfortable with. You can always make adjustments at the register.

Reserve higher tips for special situations. This might be rewarding a worker at your favorite coffee shop, or showing your appreciation when someone provides extra-special service.

Don’t feel bound by on-screen tip recommendations. Use the “custom” tip option when available to leave the amount you want.

Carry small bills. These can be used in traditional tip jars, or when traveling, to reward workers who don’t have access to digital tips.

Talk to the manager or business owner if you have questions or complaints. It’s not always clear where your tips are going (for example at fast-casual restaurants or when ordering online), so feel free to ask. And reserve your complaints about tipping expectations for management, rather than workers.

Respect policies. While many businesses encourage tipping, some do not allow their employees to accept tips for legal reasons. Instead, consider leaving positive feedback.

1) Pew Research Center, 2023

2) Toast, 2023; American Hotel & Lodging Association, 2023; U.S. News & World Report, 2023

IMPORTANT DISCLOSURES

The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Securities and investment advice offered through Investment Planners, Inc. (Member FINRA/SIPC) and IPI Wealth Management, Inc., 226 W. Eldorado Street, Decatur, IL 62522. 217-425-6340.

Social Security is complex, and the details are often misunderstood even by those who are already receiving benefits. It’s important to understand some of the basic rules and options and how they might affect your financial future.

Full retirement age (FRA)

Once you reach full retirement age, you can claim your full Social Security retirement benefit, also called your primary insurance amount or PIA. FRA ranges from 66 to 67, depending on your birth year (see chart).

Claiming early

The earliest you can claim your Social Security retirement benefit is age 62. However, your benefit will be permanently reduced if claimed before your FRA. At age 62, the reduction would be 25% to 30%, depending on your birth year. Your benefit may be further reduced temporarily if you work while receiving benefits before FRA and your income exceeds certain levels. However, when you reach FRA, an adjustment is made, and over time you will regain any benefits lost due to excess earnings.

Claiming later

If you do not claim your benefit at FRA, you will earn delayed retirement credits for each month you wait to claim, up to age 70. This will increase your benefit by two-thirds of 1% for each month, or 8% for each year you delay. There is no increase after age 70.

Spousal benefits

If you’re married, you may be eligible to receive a spousal benefit based on your spouse’s work record, whether you worked or not. The maximum spousal benefit, if claimed at your full retirement age, is 50% of your spouse’s PIA (regardless of whether he or she claimed early) and doesn’t include delayed retirement credits. If you claim a spousal benefit before reaching your FRA, your benefit will be permanently reduced.

Dependent benefits

Your dependent child may be eligible for benefits after you begin receiving Social Security if he or she is unmarried and meets one of the following criteria: (a) under age 18, (b) age 18 to 19 and a full-time student in grade 12 or lower, (c) age 18 or older with a disability that started before age 22. The maximum family benefit is equal to about 150% to 180% of your PIA, depending on your situation.

Survivor benefits

If your spouse dies, and you have reached your FRA, you can claim a full survivor benefit — 100% of your deceased spouse’s PIA and any delayed retirement credits. Note that FRA is slightly different for survivor benefits: 66 for those born from 1945 to 1956, gradually rising to 67 for those born in 1962 or later.

Claiming Early or Later

You can claim a reduced survivor benefit as early as age 60 (age 50 if you are disabled, or at any age if you are caring for the deceased’s child who is under age 16 or disabled, and receiving benefits). If you are eligible for a survivor benefit and a retirement benefit based on your own work record, you could claim a survivor benefit first and switch to your own retirement benefit at your FRA or later, if it would be higher.

Dependent children are eligible for survivor benefits, using the same criteria as dependent benefits. Dependent parents age 62 and older may be eligible for survivor benefits if they received at least half of their support from the deceased worker at the time of death.

Divorced spouses

If you were married for at least 10 years and are unmarried, you can receive a spousal or survivor benefit based on your ex’s work record. If your ex is eligible for but has not applied for Social Security benefits, you can still receive a spousal benefit if you have been divorced for at least two years.

These are just some of the fundamental facts to know about Social Security. For more information, including an estimate of your future benefits, see ssa.gov.

IMPORTANT DISCLOSURES

The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Securities and investment advice offered through Investment Planners, Inc. (Member FINRA/SIPC) and IPI Wealth Management, Inc., 226 W. Eldorado Street, Decatur, IL 62522. 217-425-6340.

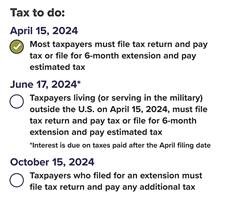

Tax filing season is here again. If you haven’t done so already, you’ll want to start pulling things together — that includes getting your hands on a copy of your 2022 tax return and gathering W-2s, 1099s, and deduction records. You’ll need these records whether you’re preparing your own return or paying someone else to prepare your tax return for you.

Don’t procrastinate. The filing deadline for individuals is generally Monday, April 15, 2024.

Filing for an extension

If you don’t think you’re going to be able to file your federal income tax return by the due date, you can file for and obtain an extension using IRS Form 4868, Application for Automatic Extension of Time to File U.S. Individual Income Tax Return. Filing this extension gives you an additional six months (to October 15, 2024) to file your federal income tax return. You can also file for an extension electronically — instructions on how to do so can be found in the Form 4868 instructions.

Due Dates for 2023 Tax Returns

Filing for an automatic extension does not provide any additional time to pay your tax. When you file for an extension, you have to estimate the amount of tax you will owe and pay this amount by the April filing due date. If you don’t pay the amount you’ve estimated, you may owe interest and penalties. In fact, if the IRS believes that your estimate was not reasonable, it may void your extension.

Note: Special rules apply if you’re living outside the country or serving in the military and on duty outside the United States. In these circumstances, you are generally allowed an automatic two-month extension (to June 17, 2024) without filing Form 4868, though interest will be owed on any taxes due that are paid after the April filing due date. If you served in a combat zone or qualified hazardous duty area, you may be eligible for a longer extension of time to file.

What if you owe?

One of the biggest mistakes you can make is not filing your return because you owe money. If your return shows a balance due, file and pay the amount due in full by the due date if possible.

If there’s no way that you can pay what you owe, file the return and pay as much as you can afford. You’ll owe interest and possibly penalties on the unpaid tax, but you’ll limit the penalties assessed by filing your return on time, and you may be able to work with the IRS to pay the remaining balance (options can include paying the unpaid balance in installments).

Expecting a refund?

The IRS has stepped up efforts to combat identity theft and tax refund fraud. More aggressive filters that are intended to curtail fraudulent refunds may inadvertently delay some legitimate refund requests. In fact, the IRS is required to hold refunds on all tax returns claiming the earned income tax credit or the additional child tax credit until at least February 15.

Most filers, though, can expect a refund check to be issued within 21 days of the IRS receiving a tax return. However, note that in recent years the IRS has experienced delays in processing paper tax returns.

So if you are expecting a refund on your 2023 tax return, consider filing as soon as possible and filing electronically.

IMPORTANT DISCLOSURES

The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Securities and investment advice offered through Investment Planners, Inc. (Member FINRA/SIPC) and IPI Wealth Management, Inc., 226 W. Eldorado Street, Decatur, IL 62522. 217-425-6340.

Couples who have opposite philosophies regarding saving and spending often have trouble finding common ground, and money arguments frequently erupt. But you can learn to work with — and even appreciate — your financial differences.

Money habits run deep

If you’re a saver, you prioritize having money in the bank and investing in your future. You probably hate credit card debt and spend money cautiously. Your spender spouse may seem impulsive, prompting you to think, “Don’t you care about our future?” But you may come across as controlling or miserly to your spouse who thinks, “Just for once, can’t you loosen up? We need some things!”

Such different outlooks can lead to mistrust and resentment. But are your characterizations fair? Money habits run deep, and have a lot to do with how you were raised and your personal experience. Instead of assigning blame, focus on finding out how each partner’s financial outlook evolved.

Saving and spending actually go hand in hand. Whether you’re saving for a vacation, a car, college, or retirement, your money will eventually be spent on something. You just need to decide together how and when to spend it.

Talk through your differences

Sometimes couples avoid talking about money because they are afraid to argue. But scheduling regular money meetings could give you more insight into your finances and provide a forum for handling disagreements, helping you avoid future conflicts.

You might not have an equal understanding of your finances, so start with the basics. How much money is coming in and how much is going out? Next, work on discovering what’s important to each of you.

To help ensure a productive discussion, establish some ground rules. For example, you might set a time limit, insist that both of you come prepared, and take a break if the discussion becomes too heated. Communication and compromise are key. Don’t just assume you know what your spouse is thinking — ask, and keep an open mind.

Here are some questions to get started.

What’s Your Money Style?

Source: Consumer Financial Protection Bureau

Agree on a plan

Once you’ve explored what’s important to you, create a concrete budget or spending plan that will help keep you on the same page. For example, to account for both perspectives, you could make savings an “expense” and also include a “just for fun” category. If a formal budget doesn’t work for you, find other ways to blend your styles, such as automating your savings or bill paying, prioritizing an emergency account, or agreeing to put specific percentages of your income toward wants, needs, and savings.

And track your progress. Scheduling money dates to go over your finances will give you a chance to celebrate your successes or identify what needs to improve. Be willing to make adjustments if necessary. It’s hard to break out of patterns, but with consistent effort and good communication, you’ll have a strong chance of finding the middle ground.

IMPORTANT DISCLOSURES

The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Securities and investment advice offered through Investment Planners, Inc. (Member FINRA/SIPC) and IPI Wealth Management, Inc., 226 W. Eldorado Street, Decatur, IL 62522. 217-425-6340.